NZDD Stablecoin and the Next Phase of Digital Payments in New Zealand

NZDD, New Zealand's dollar-pegged stablecoin, has become a bigger topic of discussion in 2026. A major reason was the decision by the Financial Markets Authority (FMA) in March, which confirmed that NZDD is not considered a financial product under current law.

The ruling gave the project greater regulatory certainty and drew attention to the role stablecoins could play in the country's payment system. As interest in digital payments continues to grow, NZDD is now being viewed as an example of how digital currencies might fit within New Zealand's existing legal framework.

What Is NZDD and Why Does It Matter?

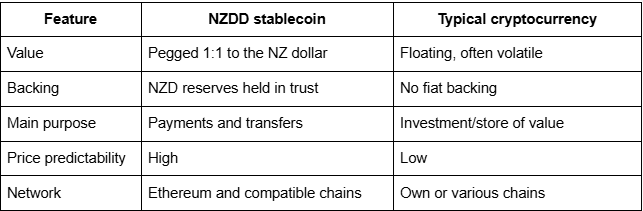

A stablecoin is a digital token meant to keep a steady value by linking it to a stable asset. NZDD is pegged one-to-one to the New Zealand dollar, with each token backed by an equivalent NZD held in a bare trust at a New Zealand-registered bank for token holders.

NZDD is issued by ECDD Holdings Limited and is part of Easy Crypto’s ecosystem, with technical development supported by an Australian blockchain firm. It operates on Ethereum and compatible networks, can be stored in standard Ethereum wallets, and is available through selected exchanges. Its combination of local-currency stability and blockchain functionality distinguishes it from typical cryptocurrencies.

Using NZDD is simple because its value stays tied to the New Zealand dollar, so users don’t have to worry about sudden changes. It works well for payments, transfers, and online shopping. For online casinos, NZDD can make deposits and withdrawals faster and more predictably. Players can focus on the benefits of a casino bonus, like extra spins or bonus funds, without worrying that slow or unreliable payments will get in the way.

The Impact of the FMA's 2026 Ruling

On 11 March 2026, the FMA officially confirmed that NZDD is not a financial product under the Financial Markets Conduct Act 2013. The regulator concluded that NZDD does not work like an investment because it pays no interest or income to holders. Instead, it functions as a way to transfer and store money digitally. This was the first designation of its kind in New Zealand and gave NZDD a clear regulatory status.

The decision applies only to NZDD and should not be seen as a ruling for all stablecoins. At the same time, the FMA continues to explore how digital assets should be regulated in the future. Data released by the issuer showed that more than 820,000 NZDD tokens were in circulation in 2024, backed by over NZ$830,000 held in reserve. For businesses and consumers, the main result of the 2026 ruling is greater certainty about how NZDD fits within New Zealand's existing legal framework.

How Stablecoins Could Transform Digital Payments

While the long-term impact of NZDD is still uncertain, stablecoins could change how digital payments work in the future. Because they operate on blockchain networks, transfers can be processed at any time of day and are not limited by traditional banking hours. This could make payments faster and, in some cases, reduce costs for both businesses and consumers.

Some of the potential benefits include:

Faster transfers, often completed within minutes

Lower costs for certain international payments

Automated payments through smart contracts

Access to funds 24 hours a day, seven days a week

An additional payment option for merchants, alongside cards and bank transfers

These possibilities are still developing. How widely stablecoins are used will depend on regulation, business adoption, and how comfortable consumers feel using digital assets for everyday payments.

What NZDD Could Mean for New Zealand's Digital Economy

Fast and reliable payments are becoming more important as more services move online. New Zealand already has a high level of digital payment use. According to Stats NZ, cardholders made around 195 million electronic card transactions in December 2025 alone, showing how much consumers and businesses rely on digital payments in their daily activities.

Against this backdrop, NZDD provides an example of how a New Zealand dollar-backed digital currency could fit within the country's existing legal framework. If stablecoins gain wider acceptance, they could offer another way to move money online alongside bank transfers and card payments.

The FMA's 2026 ruling does not guarantee widespread adoption, but it does provide greater certainty for businesses exploring digital payment options. As digital commerce continues to grow, payment methods that combine speed, transparency, and regulatory clarity are likely to attract increasing attention.

Conclusion

NZDD has become an important example of how digital currencies can fit within New Zealand's existing rules. The FMA's 2026 decision confirmed that the stablecoin should be treated as a payment product rather than an investment, giving businesses and consumers a clearer understanding of how it can be used. While the ruling applies only to NZDD, it shows that a New Zealand dollar-backed stablecoin can operate within the current legal framework. As digital payments continue to grow, the case is likely to play a role in future discussions about stablecoins, fintech innovation, and the future of money in New Zealand.